Your tax return will show you your total income, your adjusted gross income, and your taxable income, but those numbers don’t show the most important figure of all.

Your tax return will show you your total income, your adjusted gross income, and your taxable income, but those numbers don’t show the most important figure of all.

Your “taxable income” is meaningless.

So what’s the most important number the IRS doesn’t care about but you should?

Your net profit.

It’s not what you make; it’s what you keep.

What’s your net profit for the year? What’s left over after ALL your expenses, not just the deductible ones?

Your net profit figure is irrelevant to Uncle Sam but super-relevant to side hustlers and anyone else with financial freedom on their “to-do” list.

The family that makes $200,000 a year but spends it all is actually worse off financially than the family earning $50,000 that spends $40,000 — even though they earn 4x as much.

Personal Profitability

In 2024, median family income was $105,000. Put another way, that’s about a $2,000 a week or $400 per business day.

But how profitable were they?

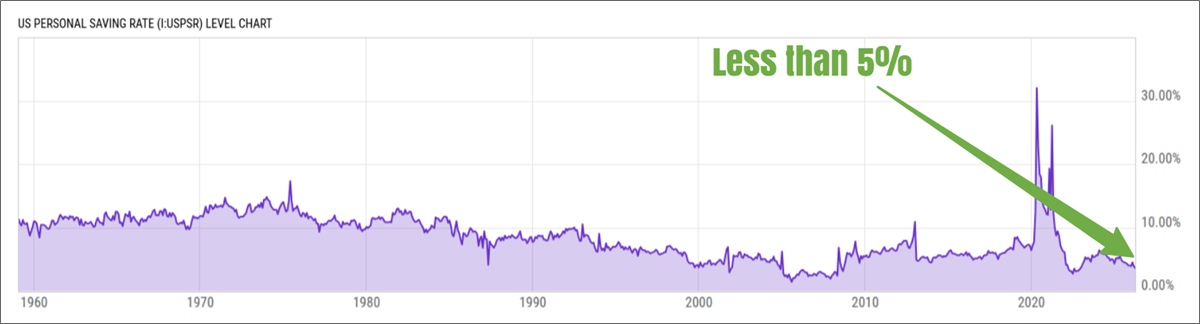

The best measure of personal profitability on a national scale is the saving rate, which is currently less than 5%.*

Does that seem low to anyone else?

This figure is generally calculated by dividing your net “disposable” income by how much you save. (And to their credit, the Bureau of Economic Analysis considers just about every take home dollar disposable.)

That means our median American family is left with $3,780 at the end of the year. (Let’s just ignore taxes for now.)

Or put another way, we work all week and make — truly make — about $72.

Is it worth it? The 40+ hours, the commute, the drama, the car, the house? For $72 added to your personal bottom line?

And even added up for 12 months, that $3,780 isn’t much of a cushion against hard times, unexpected expenses, or to put toward bootstrap seed money or retirement savings.

Have you ever calculated your “personal profitability” before?

I think it’s a hugely overlooked metric.

Why Your Personal Net Profit Matters

The greater your saving rate, the faster you reach financial freedom.

Now clearly the more you earn the easier it becomes to sock money away, but personal profitability is simply living below your means — at any income level.

Remember the Rich Dad definition of escaping the rat race? It’s when income from assets exceeds your monthly expenses. That could be business or investment income.

Could you save 10%? 20%? 50%? How many years could you shave off your career by becoming more profitable?

Our median family with an average saving rate has annual expenses of $50,867. (If they save 5.2% of their earnings, they spend 94.8% it).

Let’s call it $50k for the sake of simplicity.

According to the 4% rule, that means they need to accumulate $1.25 million in assets to retire. At their current level of profitability, and earning 8% on their savings/investments, that would take 79 years.

Ouch!

But if the family could improve their profitability, say by increasing their saving rate to 25%, they could cut 20 years off that timeline.

Sometimes the tiny tweaks make a big impact.

And if you’re not excited by a 59-year waiting period (I can’t blame you!), remember this only addresses one side of the equation. There’s only so much spending you can cut, but there’s an unlimited upside on how much you can earn.

How to Find Your Net Profit – Even If You’re an Employee

Calculating your personal net profit is simple, but not necessarily easy.

The basic equation is the same as it is for any business:

Revenue – Expenses = Profit

Revenue, or your income, is relatively easy to figure out. You probably already know how much you earn with each paycheck. Add in your side hustle income and any investment income and you’ve got your top-line number.

Expenses are trickier. I rely on annual summary statements from my credit card providers to get most of the data, because I spend very little cash.

If you want to be very meticulous about it, you can track every expense in a notepad or in Excel.

Try it for a month.

Example:

$4,000 salary + $500 side hustle – $2,500 expenses = $2,000 monthly profit

Note: I’ll argue, like Joshua Sheats did, that taxes ARE part of your profitability. You can choose where you live, and some cities/states/countries are more favorable than others.

Start Thinking Like a CEO

You’re the CEO of your own life. You’re in control, even if doesn’t feel like it right now.

And it’s your job to care about your personal profitability because no one else will do it for you.

The buck stops here!

What can you do to improve your bottom line? Earn more? Spend less? Both?

Your Turn

Crunch your numbers and see what you come up with. Did you beat the “average” saving rate of 5.2% last year?

Comment below to see how your personal profitability stacks up against the rest of Side Hustle Nation!

************

*Economists might point to a different metric, gross savings as a percentage of GDP. At last measure, that figure painted a rosier picture for American families at 18%.

Wow! As a freelancer myself, I never thought about the idea of profitability as it relates to my career. I didn’t crunch numbers but I think I should. Thank you for a great and informative article!

One of your best posts, Nick. I want to add some do-as-I-say-not-do-as-I-did advice: pay very close attention to your biggest spending category, the home you live in. I’m sitting right now in a house we’re trying to get rid of (this is why, just for once, I’m Anonymous) which has cost us a fortune over the years.

Now, we got this house for the sake of the children–we were looking for the right school district, nice big bedrooms for them, a big finished basement for those teen years–and in that we succeeded. Our kids got a privileged upbringing I could never have dreamed of. It’s natural to want to do that for your kids–you’ll reach that point sooner than you think!

But it cost us. We spent money we could have been saving for our own financial freedom, and worse, we remained in debt (mostly mortgage) when we could have gotten out much earlier. And we’re less extravagant than most of our neighbors, who spend huge $$$ on looking good. We’ve been fortunate and have managed to avoid disaster, but that’s not true of several of the people who have their houses on the market right now.

So my advice to the side hustlers out there is–buy the smaller house. Aim for minimal debt levels, or none at all if you can. I think your generation thinks far more like that than mine does, so perhaps I’m preaching to the choir? I hope so.

Brilliant Nick, just brilliant.

Exactly why I quit my solid 6-figure job to run my own business and actually have money left over, even with making SUBSTANTIALLY Less ;)

Woohoo congrats on making the leap!

Great post! Its an interesting and motivational angle that is sure to get people to thinking about their money. My wife and I currently save nearly twice as much money as we spend each month, so I feel like we are doing fairly well in regards to profitablity. The bad news? Virtually all of that profit comes from our employers… We have no viable side hustles at the moment. We did start P2P lending recently and are currently trying to decide on a side hustle to help us along the path to exiting the rat race. Keep the ideas coming Nick!

Personal Profitability is all about earning more, spending thoughtfully, growing your wealth, and living a better life through mindful personal finance. It is good to spend money on a property or buying different assets and to manage them.